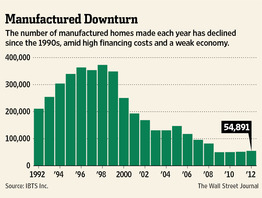

“Loans with rates and fees above certain thresholds are supposed to be designated ‘high cost’ by the Consumer Financial Protection Bureau and thus subject to fewer legal protections. The bureau earlier this year decided to call loans high-cost if they have an annual percentage rate of more than 6.5 percentage points above a national average and 8.5 percentage points for many loans under $50,000. Lenders to manufactured-home buyers say many of their loans would fall into the high-cost category with this regulation, which goes into effect in January. They warn that they won’t make such loans because they carry increased legal risk.”

http://online.wsj.com/article/SB10001424127887323551004578440900357683558.html

Did you like this?

Tip Freedomwat.ch Staff with Bitcoin

Tip Freedomwat.ch Staff with Bitcoin

Related posts:

Donald Trump eyeing ‘building swap’ for FBI headquarters

Oklahoma state legislator introduces bill to banish NSA

The Hole in Our Collective Memory: How Copyright Made Mid-Century Books Vanish

State seizes couple's four babies due to father's juvenile sex offense

Will SoFi Take Sallie Mae's Best Customers?

Kenya, home to Africa's ‘Silicon Valley’, is set to be the continent's tech hub

Be Very Careful, Beloved Spain

Federal Reserve Monetary Policy To Target Wealth Inequality?

India central bank lifts ban on import of gold coins, medallions by banks

Snapchat's young users snap up stock — and want more IPOs

Foreign embassies in London hard hit as HSBC closes their bank accounts

NATO kills four children in Afghan East: Karzai

Dubai offers gold to fight obesity epidemic

King of My Castle? Yeah, Right

Declassified files reveal US supported Indonesia's fascist massacre