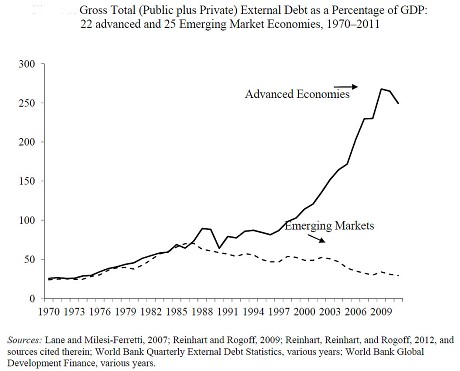

“Much of the Western world will require defaults, a savings tax and higher inflation to clear the way for recovery as debt levels reach a 200-year high, according to a new report by the International Monetary Fund. The IMF working paper said debt burdens in developed nations have become extreme by any historical measure and will require a wave of haircuts, either negotiated 1930s-style write-offs or the standard mix of measures used by the IMF in its ‘toolkit’ for emerging market blow-ups. Financial repression can take many forms, including capital controls, interest rate caps or the force-feeding of government debt to captive pension funds and insurance companies.”

Did you like this?

Tip Freedomwat.ch Staff with Bitcoin

Tip Freedomwat.ch Staff with Bitcoin

Related posts:

Marc Faber - CNBC TV 18 - 06 Aug 2012

Al Franken Leaning Toward Supporting Syria Resolution

Want to play the market? Count the Fed leak weeks

9 NYC Stores Fined for Propping Air-Conditioned Doors Open [2010]

Military estimates 500 sexual assaults per week

The Ron Paul Channel: libertarianism 'unfiltered and uninterrupted'

Swiss pilot cleared to finish solar plane trek across U.S.

UN: New generation of secret British courts could conceal torture collusion

Restaurant Shift: Sorry, Just Part-Time

Fed Prez Spills the Beans on the Excess Reserve Inflation Time Bomb

Target stores attacked by pornographic pranksters

Syrian President Bashar al Assad - Charlie Rose Interview 9/9/2013

Teenagers buying China stocks may indicate serious bubble

Swiss government blocks arms sales to U.S. over human rights concerns

Congress poised to jam through reauthorization of mass surveillance