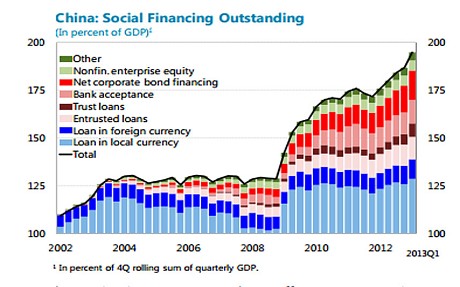

“As you can see from the first chart, total credit has jumped from 129pc to 195pc of GDP since 2008, and has completely departed from its historic trend. The great mistake, plainly, was to keep the foot on the floor in 2010 and 2011, long after the Lehman crisis had subsided. The deeper thrust of the IMF report is that the growth model of the past 30 years is exhausted. The low-hanging fruit has been picked. If the Communist Party fails to take radical action, it will soon be caught in the middle income trap. Loans have jumped from $9 trillion to $23 trillion since 2008, a faster pace of debt build-up than in any major episode of the past century.”

Did you like this?

Tip Freedomwat.ch Staff with Bitcoin

Tip Freedomwat.ch Staff with Bitcoin

Related posts:

'Rejoice: the Yellen Fed will print money forever to create jobs'

Centuries-old disfiguring plague breaks out due to the war in Syria

Saudi Prince says Bitcoin is ‘just going to implode one day’

Australia to Fly Guns and Ammunition Into Iraq

Two Accused of Kidnapping a Chinese Student and Trying to Deport Him

Snowden Gets Whistleblower Award in Germany

Fund Manager Hugh Hendry: I would buy Bitcoin if I could

Bitcoin: how I made a virtual fortune

In an age of e-commerce, the 'Quill rule' is more vital than ever

Residents, politicians push to shut Satoshi Forest homeless camp

California school district pays $650,000 to settle police brutality & false arrest case

Uber’s First Self-Driving Fleet Arrives in Pittsburgh This Month

Egypt orders arrest of ousted Brotherhood leaders after army kills 53 protesters

Treasury Department: Legally-married same sex couples qualify to file joint taxes

British couple who helped Kenyan village with cannabis profits jailed