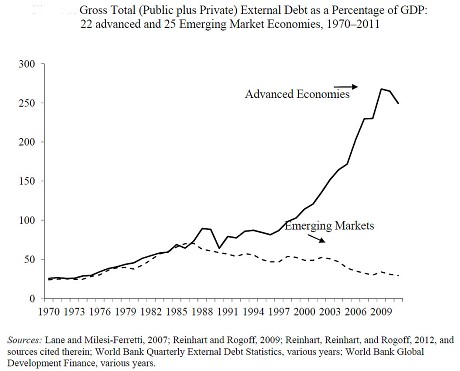

“Much of the Western world will require defaults, a savings tax and higher inflation to clear the way for recovery as debt levels reach a 200-year high, according to a new report by the International Monetary Fund. The IMF working paper said debt burdens in developed nations have become extreme by any historical measure and will require a wave of haircuts, either negotiated 1930s-style write-offs or the standard mix of measures used by the IMF in its ‘toolkit’ for emerging market blow-ups. Financial repression can take many forms, including capital controls, interest rate caps or the force-feeding of government debt to captive pension funds and insurance companies.”

Did you like this?

Tip Freedomwat.ch Staff with Bitcoin

Tip Freedomwat.ch Staff with Bitcoin

Related posts:

Kerry blames Iran for attack on Iraq camp

Are giant bubbles the key to beating Beijing’s pollution?

Switzerland and Britain are now at currency war

At least 70 supporters of Mohamed Morsi killed by security services in Cairo

Wall Street Journal’s Chinese version site blocked in China

Credit card firm cuts off nation's No. 1 gun store --- for selling guns

Secret U.S. documents reveal Al-Qaeda has anti-drone operation

Fed fears risks posed by exit tools; plan almost done

China is mining data directly from workers’ brains on an industrial scale

U.S. Will Now Let in A Whole 2,000 Syrian Refugees Per Year

China tops world in gold producing

US-Backed Saudi Coalition Should Lift Its Yemen Blockade

Bitcoin ATMs coming soon

Yes, Bitcoin Enables Drug Dealing, Just as Major Banks Do

Somalis Face a Snag in Lifelines From Abroad