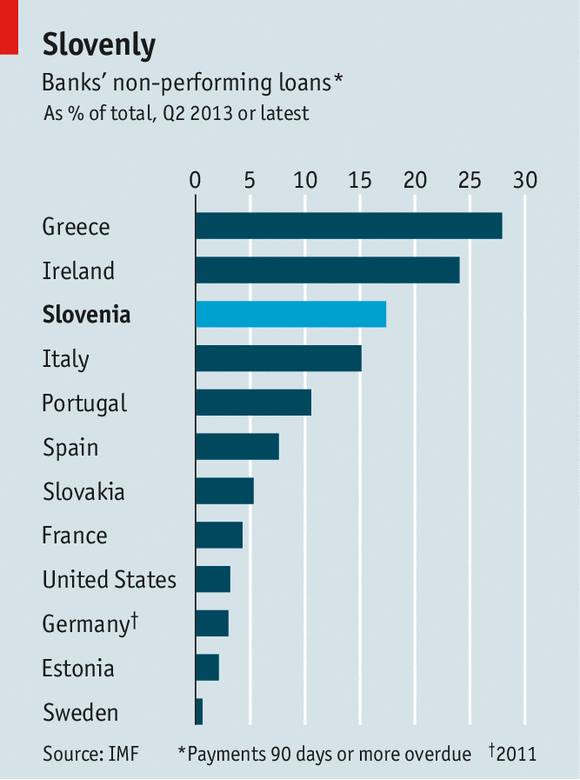

“The government of Slovenia, insists Alenka Bratusek, the prime minister of eight months, can set its country’s finances to rights without having to seek a bail-out from the euro zone and the IMF. Whether she is right will soon be revealed. In early December an independent audit and stress tests of the country’s troubled banks will disclose just how short of capital they are. Between the middle of 2012 and of 2013, the ratio of non-performing to total loans rose from 13.2% to 17.4%, which is the highest level in the euro zone after Greece and Ireland. The bad debts have been incurred predominantly through lending to businesses. ”

Did you like this?

Tip Freedomwat.ch Staff with Bitcoin

Tip Freedomwat.ch Staff with Bitcoin

Related posts:

China-U.S. Visa Deal a Problem for U.S. Immigration Consultants

Country Time Lemonade to help pay fines, permit fees for kids' lemonade stands

Fidel Castro denies Cuba refused Edward Snowden asylum

Stossel: Bitcoin revolution

Yale opens campus in Singapore, citing need for ‘critical thinking’ in Asian countries

Has military Keynesianism come to an end?

Watching you: When and where you may be tracked

Bernanke urges Congress to lift debt ceiling

Even Ivy Leaguers default on student loans

Czech artist gives president 33-foot-high one-finger salute

IMF Approves Reserve-Currency Status for China's Yuan

Nick Clegg's wealth tax is latest plan to make rich pay more

Georgia rebuilds Stalin monuments

Spain: This Is What A Permanent Underclass Looks Like

Money hidden in pastries confiscated in Germany