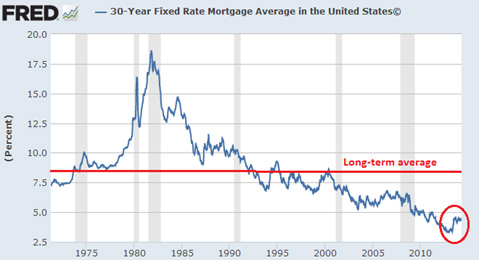

“The refinancing game is nearly over. Just looking at the mortgage side of life, this means that the increase of households’ retained cash flow is unlikely to improve further. For many of the large lenders, it also means a reduction in workforce—a significant one, in many cases—which will impact employment figures and possibly further recovery. A final note in this saga pertains to household leverage. Common wisdom seems to hold that US households have deleveraged since the mid-2000s crash. Unfortunately, that’s not the case. In 2008, total household liabilities stood around $14.2 trillion. At the end of 2013, they were $13.8 trillion—a paltry 2.8% decline.”

Did you like this?

Tip Freedomwat.ch Staff with Bitcoin

Tip Freedomwat.ch Staff with Bitcoin

Related posts:

How Nixon the Keynesian Destroyed the Monetary Regime of Keynes

Cheating to Learn: How a UCLA professor gamed a game theory midterm

Does “Homeland Security” really protect you?

The Power Elite-Obama Connection

James Bovard: Bitter lessons 25 years after Waco, Texas, siege

Canola Oil: Good or Bad?

Jeffrey Tucker: Fun and Fascinating Bitcoin

Name That Black Swan

Bruce Schneier: Why are we spending $7 billion per year on TSA?

The True Value of Bitcoin

14 Questions People Ask About How To Prepare For The Collapse Of The Economy

Yes, We Live in a Communist Country

Digital Diversification: How to Do It

Sibel Edmonds Explains Who's At The Top Of The Pyramid

How to Be a YouTube Star and Beat Justin Timberlake in the Charts