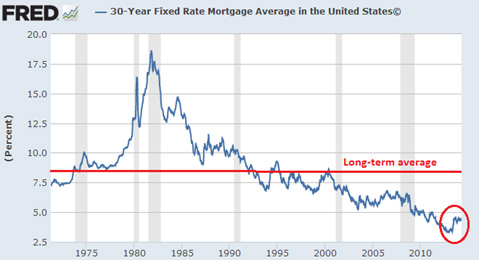

“The refinancing game is nearly over. Just looking at the mortgage side of life, this means that the increase of households’ retained cash flow is unlikely to improve further. For many of the large lenders, it also means a reduction in workforce—a significant one, in many cases—which will impact employment figures and possibly further recovery. A final note in this saga pertains to household leverage. Common wisdom seems to hold that US households have deleveraged since the mid-2000s crash. Unfortunately, that’s not the case. In 2008, total household liabilities stood around $14.2 trillion. At the end of 2013, they were $13.8 trillion—a paltry 2.8% decline.”

Did you like this?

Tip Freedomwat.ch Staff with Bitcoin

Tip Freedomwat.ch Staff with Bitcoin

Related posts:

Beyond the Debt-Ceiling Debate

Secrets and Lies of the Bailout

Richard Stallman: How Much Surveillance Can Democracy Withstand?

Let’s shatter the myth on Glass-Steagall

Blind Man's Bluff: Why the Surveillance State Is Doomed

"War is the Health of The State" - Dr. Mark Thornton

The Bitcoin Central Bank's Perfect Monetary Policy

Those "Inexplicable" Paris Attacks

Central banks that trade on the stock market [2013]

All I Want For Christmas Is the End to Unnecessary War

Understand the Emergence of the Marijuana Meme - Even In China

Top Terrorism Experts Say that Mass Spying Doesn’t Work to Prevent Terrorism

Detlev Schlichter: ‘Positive Money’ and the fallacy of the need for a state money producer

Paul Craig Roberts: Growing Up In America

The State, Not Manning, is the Criminal