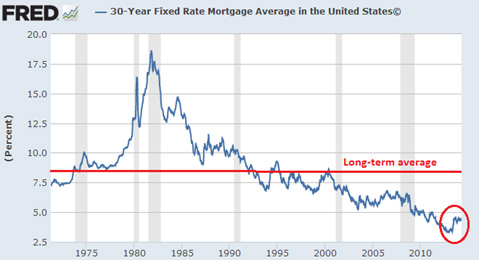

“The refinancing game is nearly over. Just looking at the mortgage side of life, this means that the increase of households’ retained cash flow is unlikely to improve further. For many of the large lenders, it also means a reduction in workforce—a significant one, in many cases—which will impact employment figures and possibly further recovery. A final note in this saga pertains to household leverage. Common wisdom seems to hold that US households have deleveraged since the mid-2000s crash. Unfortunately, that’s not the case. In 2008, total household liabilities stood around $14.2 trillion. At the end of 2013, they were $13.8 trillion—a paltry 2.8% decline.”

Did you like this?

Tip Freedomwat.ch Staff with Bitcoin

Tip Freedomwat.ch Staff with Bitcoin

Related posts:

Anthony Gregory: The Bellicosity of a Democrat’s Second Term

Khan Academy's Challenge to State-Certified Educators

Who Needs an Official State Media When We’ve Got CNN?

Jeffrey Tucker: Is There A Viable Alternative To College?

How to Use Sex Like a Russian Spy

Extremely Serious Privacy Problem in America

Will Grigg: "Damned from Memory": When the Drug War Turns on its Own

Doug Casey on Opting-Out

Canola Oil: Good or Bad?

The Holocaust, the West, and the Lost Caribbean Shelter

Creating a Culture of Denunciation

Should You Invest in the Marijuana Boom?

Bill Bonner: Is It Time To Sell Your Gold?

Doug Casey Refutes Common Hesitations to Internationalize

Criminal Enterprise Operations of the Police