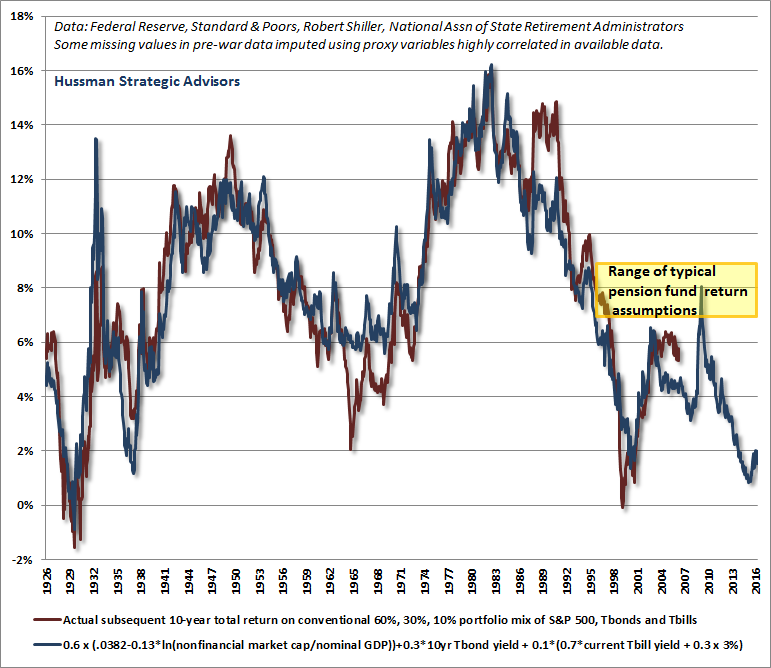

“What’s quite unfortunate, in my view, is that the strong realized past returns of the past 25 years are now actually being taken as a justification of current, unrealistically high pension return assumptions. This, in turn, encourages continued underfunding. This inclination appears to be wholly encouraged by Federal Reserve policies, and threatens to amplify an inevitable pension crisis in the coming years. The realized past returns of this period have been strong precisely because they have robbed from future expected returns. The tide will turn, as it always has in complete market cycles across history, and as investors discovered during the market collapses of 2000-2002 and 2007-2009.”

http://www.hussmanfunds.com/wmc/wmc160523.htm

Did you like this?

Tip Freedomwat.ch Staff with Bitcoin

Tip Freedomwat.ch Staff with Bitcoin